During the pandemic, the housing market in the UK boomed. While this was great news for some, housing booms lead to increased prices, which we’ve already seen across the whole of the UK, with averages increasing by over 10% in 2021 (The Guardian).

Estate agents, economists and financial commentators seem to be split on whether increases in price will continue in 2022, but one thing we already know for sure is rising interest rates will lead to people forking out more than before, regardless of whether house prices increase further.

Some of the UK’s most known banks and building societies have already increased their mortgage rates for 2022, with HSBC, NatWest and Nationwide announcing increases back in November 2021 (FT.com).

This was prior to the Bank of England rising their interest base rate from 0.1% to 0.25% at the end of 2021, so with this in mind, as well as the assumption that there will be further increases this year, it’s important to know where you stand when it comes to lending.

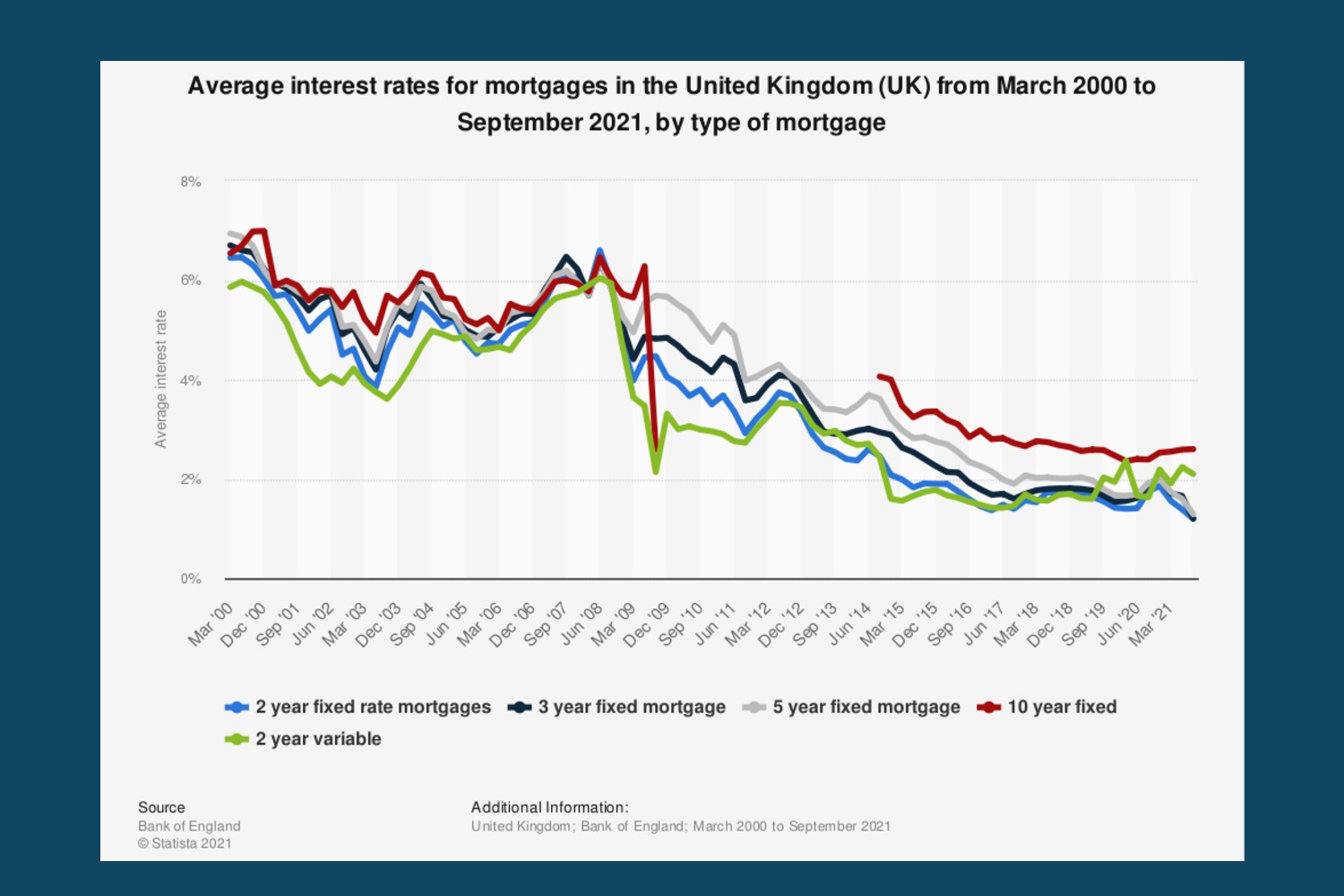

We also want to reassure our readers that an increase in interest rates isn’t necessarily cause for concern, as data by Statista and The Bank of England show mortgage rates are still considerably lower than what they were, 20 and even 10 years ago:

The UK’s Best Mortgage Rates in 2022

Within this article, you’ll not only find the best interest rates at the time of writing, but also more information about what you can expect to pay back over the duration of your loan.

Based on market insights, we’ll also offer our opinions on whether we expect the current rates to rise.

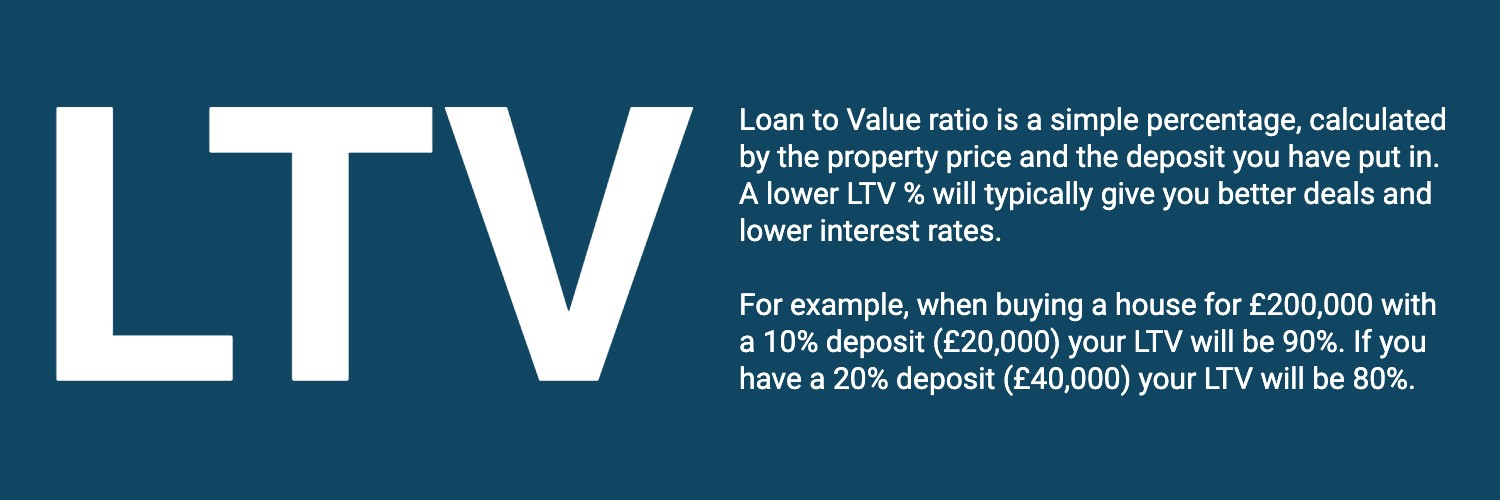

Before we get started, before purchasing a property, it’s important to understand the meaning of Loan to Value (LTV) and the impact this will have on the overall amount you will pay. Lower LTV ratios will typically give you access to lower interest rates – so the more you save for a deposit now, the less you’re going to pay overall.

The Top 8 Best UK Mortgages Rates

The average house price in the UK is now just over £250,000 so for the purpose of this article, all interest rates are based on this amount, using a 10% deposit, at £25,000 for a term of 25 years.

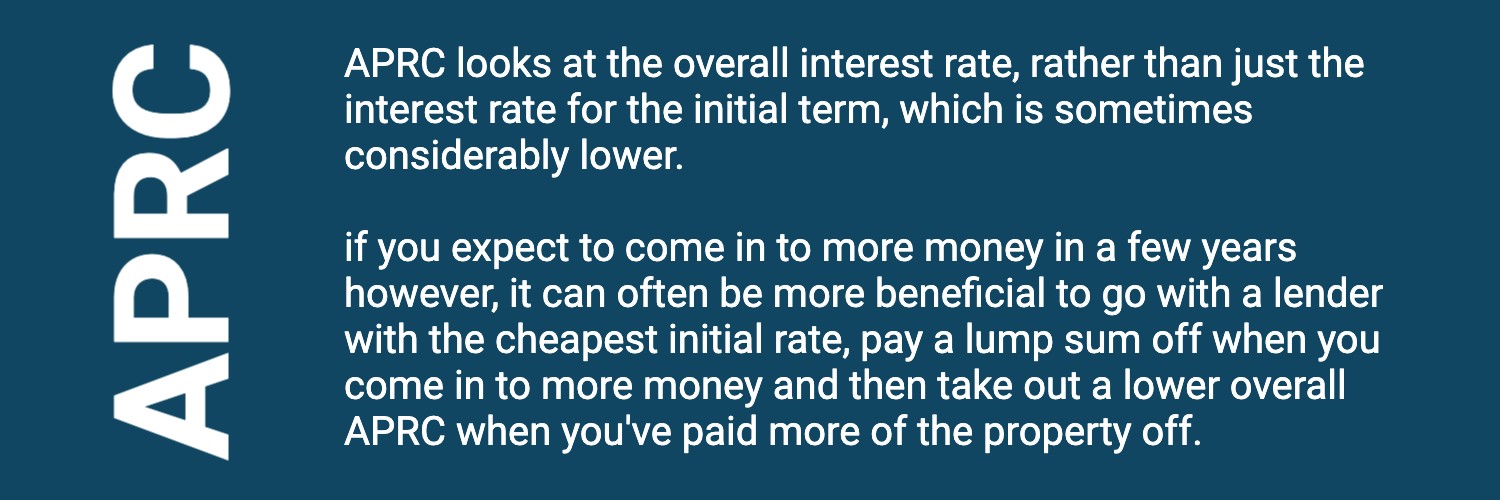

We have also based the top 8 on the APRC rate (Annual Percentage Rate of Charge) which shows you the total interest amount you’ll pay over the 25 years. Many lenders will offer a low initial interest rate to attract buyers, however it’s the APRC amount that really shows the best deal you’re getting.

1. TSB

Coming in at the current top position, with a 0.5% lead on other lenders is TSB. While a 0.5% difference may not seem like a lot, over the course of a 25 year term, you’ll save almost £18,000 in interest when comparing to the second top lender (Santander).

- Overall interest rate: 2.6%

- Overall amount payable over 25 year term (in interest and fees)*: £81,021.36

*variable interest rates may increase or decrease dependent on inflation.

2. Santander

Our second best lender at the time of writing is Santander. They are currently offering the same interest rates as our third and fourth top lenders, however the amount you’ll pay back over the course of the mortgage is slightly less. This is like due to product fees, or incentives, such as money back.

- Overall interest rate: 3.1%

- Overall amount payable over 25 year term (in interest and fees)*: £98,994.34

3. Nationwide

The third and forth best interest rates at present are from Nationwide and RBS, who offering the exact same interest rates, as well as additional product fees.

- Overall interest rate: 3.1%

- Overall amount payable over 25 year term (in interest and fees)*: £99,794.34

*variable interest rates may increase or decrease dependent on inflation.

4. RBS

As mentioned above, RBS is really in joint third position with Nationwide, with both lenders offering the same rates.

- Overall interest rate: 3.1%

- Overall amount payable over 25 year term (in interest and fees)*: £99,794.34

*variable interest rates may increase or decrease dependent on inflation.

5. First Direct

Although First Direct is a less known lender, they are competing with the UK’s biggest banks at present when it comes to interest rates.

- Overall interest rate: 3.2%

- Overall amount payable over 25 year term (in interest and fees)*: £100,299

*variable interest rates may increase or decrease dependent on inflation.

6. HSBC

Going back to the big names, HSBC comes in at the 6th position for the best current interest rates.

- Overall interest rate: 3.2%

- Overall amount payable over 25 year term (in interest and fees)*: £100,942.74

*variable interest rates may increase or decrease dependent on inflation.

7. Barclays

In joint seventh and eighth position is Barclays and Halifax, both of which are offering the same interest rates.

- Overall interest rate: 3.3%

- Overall amount payable over 25 year term (in interest and fees)*: £104,146.59

*variable interest rates may increase or decrease dependent on inflation.

8. Halifax 3.3%

- Overall interest rate: 3.3%

- Overall amount payable over 25 year term (in interest and fees)*: £104,287.24

*variable interest rates may increase or decrease dependent on inflation.

This concludes our round up of over 25 lenders, with all 8 of those we’ve featured offering interest rates under 3.5%. Some of the lenders we looked at but didn’t list are offering interest rates over 4.5%, however they may offer different benefits for going with them. Also pay attention to initial mortgage rates and APRC if your circumstances may change:

Other Mortgage Lenders to Consider in 2022

While the above mortgage rates are the best at the time of writing, there are many other lenders, many of which are lesser known, that you can also consider. While the overall interest rates are much higher, they can offer different benefits, such as lower deposits, or even consider you if you don’t have the best credit rating.

Some of the lesser known lenders include:

- Virgin Money

- Accord Mortgages

- Bank of Ireland

Final Tips on Getting the Best Rates Mortgage Rates in 2022:

- Increase your LTV ratio: Many of us can save faster than prices rise, so if it takes you an extra year to save 20%, rather than 15% of your overall property budget, this could save you a lot of money in the long run – and make you more favourable to lenders.

- Look at properties on Strike: Unlike other well-known online property websites, Strike allows sellers to upload properties themselves, by-passing the need and fees of estate agents. This has its benefits, as some people want to sell houses fast, or aren’t interested in getting the highest possible amount for it – which is always pushed by bricks and mortar estate agents.

- Lock it in: it’s advisable that if you come across an interest rate as TSBs and they’re offering fixed terms – i.e. the same rate for 5 years to secure it. We’re heading in to uncertain times, so securing a good interest rate could save you from increasing base rates in the years to come.

Want more financial advice, opinions and general money saving tips? Sign up to the Freebies newsletter to never miss an article.